How to Use a Credit Card to Build Your Credit Score (Even With a Low Limit)

Your Money Questions Answered

My credit score is 630 because I fell into the credit card trap when I turned 18 and it ended up in collections. I paid it off and the card was closed, but now I can only get a card with a $500 limit. How do I use my credit card the smart way so I can increase my credit score?

The Short Answer:

Wondering how to use a credit card to build your credit score (even with a $500 limit)?

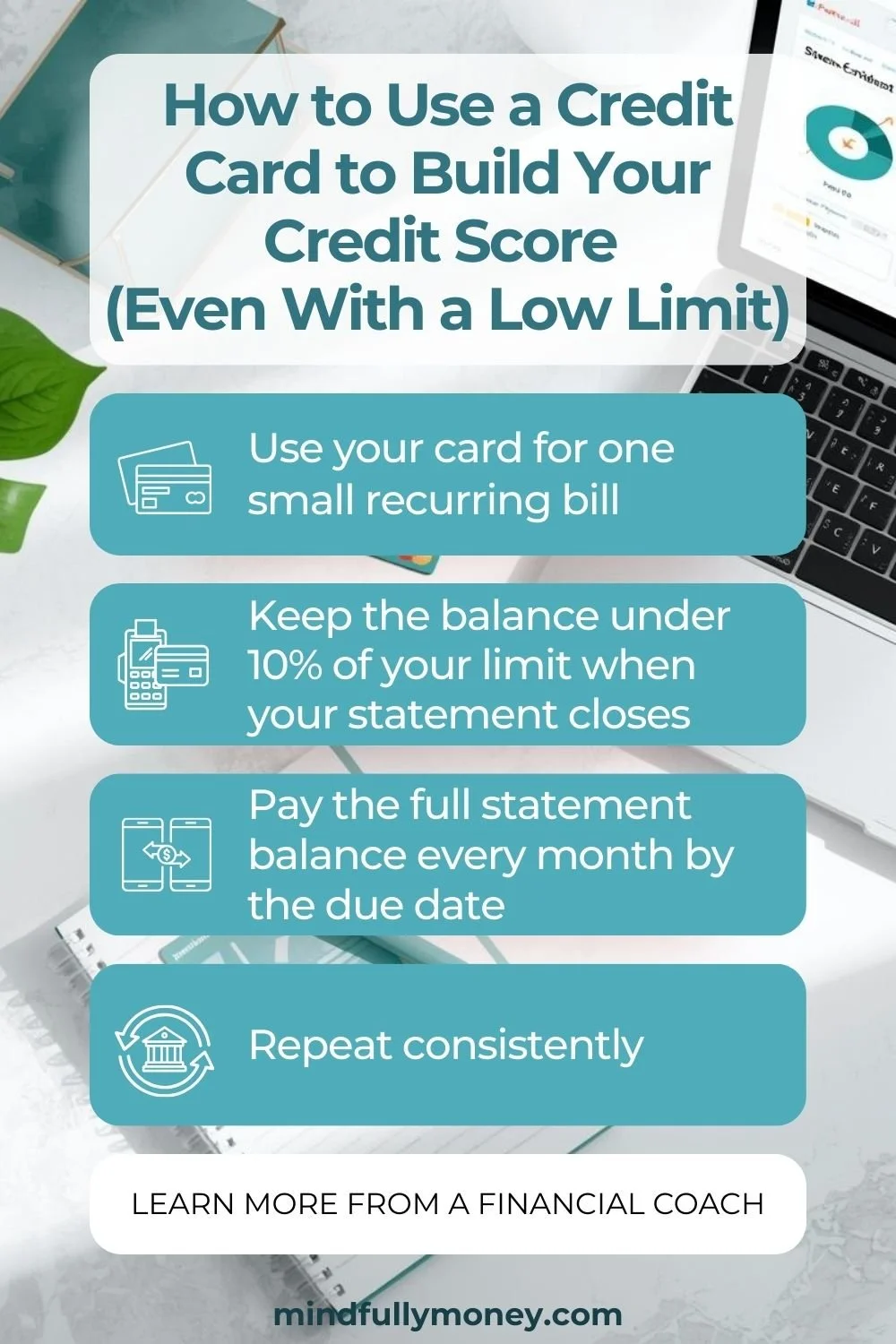

Use your card for one small recurring bill

Keep the balance under 10% of your limit when your statement closes

Pay the full statement balance every month by the due date

Repeat consistently

Even with a low credit limit, you can steadily improve your score by focusing on a few specific habits.

First of all, please don't feel bad about this. Many young people have never been taught how to manage money and then had credit cards pushed on them the moment they turned 18. (Just sign up and we'll give you this free gift!) You are so not alone in this.

Second, you're doing great by asking this question. You recognized the problem, paid off the debt, and are now thinking intentionally about how to do things differently. That's a big deal.

The good news is that even with a $500 limit, you absolutely can use that card to rebuild your score.

As a financial coach, this is one of the most common situations I help clients work through. Here's how:

How Credit Scores Actually Work

Before I get into the specifics of what to do, it helps to understand how your score actually gets calculated. There are two main factors that will matter most to you right now:

1. Credit Utilization

This is the percentage of your available credit that you're using. For example, if your card has a $500 limit and you have a $250 balance, your credit utilization is 50% ($250 ÷ $500). If your balance is $100, it's 20%.

The lower your utilization, the better. Most guidance you'll read says to keep it under 30%, and that's a reasonable starting point, but if you really want to move the needle, aim for under 10%. With a $500 limit, that means keeping your reported balance under $50.

I'll explain how to make that happen practically in a moment.

2. On-Time Payments

Credit bureaus want to see that you consistently pay what you owe. Making on-time payments is one of the most powerful things you can do to rebuild your score. Ideally, you pay the full statement balance by the due date each month — not just the minimum. (More on why that matters below.)

There are a few other factors that influence your score — length of credit history, the mix of credit types you have, and how recently you've applied for new credit — but these two are the ones most worth focusing on right now.

How to Use Your Credit Card to Build Your Credit Score

Here's what I recommend:

Pick one small recurring bill you pay every month — a streaming service, your phone bill, something under $50 if possible. This keeps your utilization low.

Set that bill to autopay to your credit card.

Don't use the card for anything else.

Set your credit card to autopay the full statement balance each month. Make sure there's always enough in your account to cover it — build this into your monthly money plan.

That's really it. You're using the card, you're showing consistent payment history, and your utilization stays low. The score will follow.

One Mistake That Trips People Up

Here's something a lot of people do that accidentally backfires: they pay their credit card off right after they use it, thinking they're being responsible.

For example, you pay your streaming service on the 15th and then pay off the credit card balance on the 16th. But if your statement closes on the 20th, the balance shows as $0. It can look like you aren’t using the card at all, which may slow down how quickly your credit improves

What gets reported to the credit bureaus is whatever balance is on your statement when it closes, not what you pay after the fact.

So the timing matters: let the statement close with a small balance on it, then pay that statement balance in full by the due date. If you set up autopay for the full statement balance, this will happen automatically — you don't have to think about it.

For more detail on how this works, read: How to Pay Your Credit Card Bill in Full Every Month. [https://www.mindfullymoney.com/blog/how-to-pay-your-credit-card-bill-in-full-every-month]

When to Ask for a Credit Limit Increase

Once you've had the card for 6 to 12 months and have established a consistent payment history, it's worth requesting a credit limit increase.

Here's why this matters: if your limit goes from $500 to $1,000, and you're still only spending $40 a month on that streaming service, your utilization drops from 8% to 4%. Your spending hasn't changed at all—but your score gets a boost because the ratio looks better.

Most card issuers let you request an increase online or by calling the number on the back of your card. Some will do a hard inquiry (a temporary small dip in your score), but many do a soft pull that doesn't affect it. It's worth asking what they'll do before you request.

Don't ask too soon—give it at least 6 months of on-time payments first. And if they say no, try again in another 6 months.

What Not to Do

A few things worth avoiding as you're rebuilding:

Don't apply for multiple new cards at once. Each application can create a small, temporary dip in your score, and opening several accounts quickly can signal risk to lenders.

Don't close the card once your score improves. Length of credit history matters, and closing a card shortens your history and reduces your total available credit (which raises your utilization ratio on any other cards you have).

Don't carry a balance to "build credit." You'll sometimes hear that carrying a small balance helps your score. It doesn't—and it costs you interest for no reason. Pay it in full every month.

For more on this: Should You Carry a Balance to Build Credit? and Smart Ways to Use Your Credit Card to Your Advantage

How Long Will This Take?

Building credit is a slow process — I want to be honest about that. With consistent on-time payments and low utilization, most people see meaningful improvement within 6 to 12 months. Getting from 630 to the 700s is very achievable within a year if you're using the card correctly and nothing negative is being added to your report.

If you want to go deeper on everything that affects your score: Learn Everything You Need to Know About Credit Scores

Frequently Asked Questions

How fast can I raise my credit score?

It depends on your starting point and what's on your report, but with consistent on-time payments and low utilization, many people see noticeable improvement within 3 to 6 months. Significant movement from the 600s into the 700s typically takes closer to 12 months.

What credit utilization should I aim for?

Under 30% is the widely cited guideline, but under 10% will have a stronger positive impact on your score. If you have a $500 limit, that means keeping your reported balance under $50 when your statement closes.

Does paying my credit card in full hurt my credit?

No. Paying in full is always the right move. The key is making sure there's a balance on your statement when it closes before you pay it. What matters to your score is what gets reported, not what you pay off afterward.

What if my credit limit is really low?

You can still build credit with a low limit (even if your limit is only $500) — you just need to be mindful of utilization. Using the card for one small recurring expense and paying it in full each month is enough. After 6 to 12 months of consistent payments, request a credit limit increase to help your utilization ratio even further.

Should I get more than one credit card to build credit faster?

Not necessarily, especially right now. One card used responsibly is enough to build credit. Adding more too quickly can trigger hard inquiries and make it look like you're in financial distress. Focus on using this one card well for at least a year before considering adding another.

Does paying my credit card early hurt my credit?

Paying early doesn’t hurt your credit—but if your balance is $0 when your statement closes, it won’t help build your score either.