How to Combine Finances in Marriage and Other Committed Relationships

Many couples who have made some sort of commitment, whether that’s getting married, moving in together, or something else, at some point start wondering how they should combine their finances—or if they should combine them at all.

This decision used to be much more straightforward—households generally just had one set of finances and accounts. The expectation in the 1950s, for example, was that two heterosexual young people got married, then moved in together, and then had kids. Divorce was frowned upon. Gay marriage was illegal. The man earned money and the wife lounged around and ate bon bons did the work of five people without getting paid.

(Now, of course, it is not uncommon for the wife to also do work for which she is paid and still do the work of five people without getting paid.)

It made sense for a family unit to have completely merged finances. After all, until the latter half of the 19th century, women couldn’t own property because they basically were property. American women weren’t even allowed to have their own bank accounts until the 1960s and 70s. So yes, it made sense… because having combined finances was the only option.

Thankfully, things have changed. There is still work to be done in terms of ensuring women have equal pay, equal opportunities, and equal standing and responsibilities in marriage, but some progress has been made.

But things are also much more complicated now (in a good way). It’s much more common to have both partners earning money, and maybe even bring significant assets into a marriage or partnership. Conversely, many people bring significant credit card debt or student loans. Those in their second (or third, or…) marriage might have children from another relationship or an obligation to pay alimony. Some choose not to get married at all (which is totally fine too!).

Relationships are complicated, and figuring out how to pay for things together or combine finances after marriage (or whatever level of commitment you’ve made) is no easy task, and there is no one right way that will work for everyone.

Here are a few things to keep in mind as you figure out which option is right for you:

It’s generally a good thing for couples to have access to their own money, particularly to protect themselves in case of divorce or separation.

Having one partner in charge of all the money creates an unfair power imbalance.

Being required to talk about every little expense or get permission to buy something is bad for a relationship (and for the individuals).

If one partner manages everything and then dies or loses the ability to manage money, there’s a risk that the other partner won’t know how to manage money.

Both partners should be involved in making decisions about money, even if only one spouse takes care of bill paying and other basic tasks.

A marriage is more than two individuals—it is a relationship. If you want to be in a relationship, you need to think beyond yourselves and create a life together.

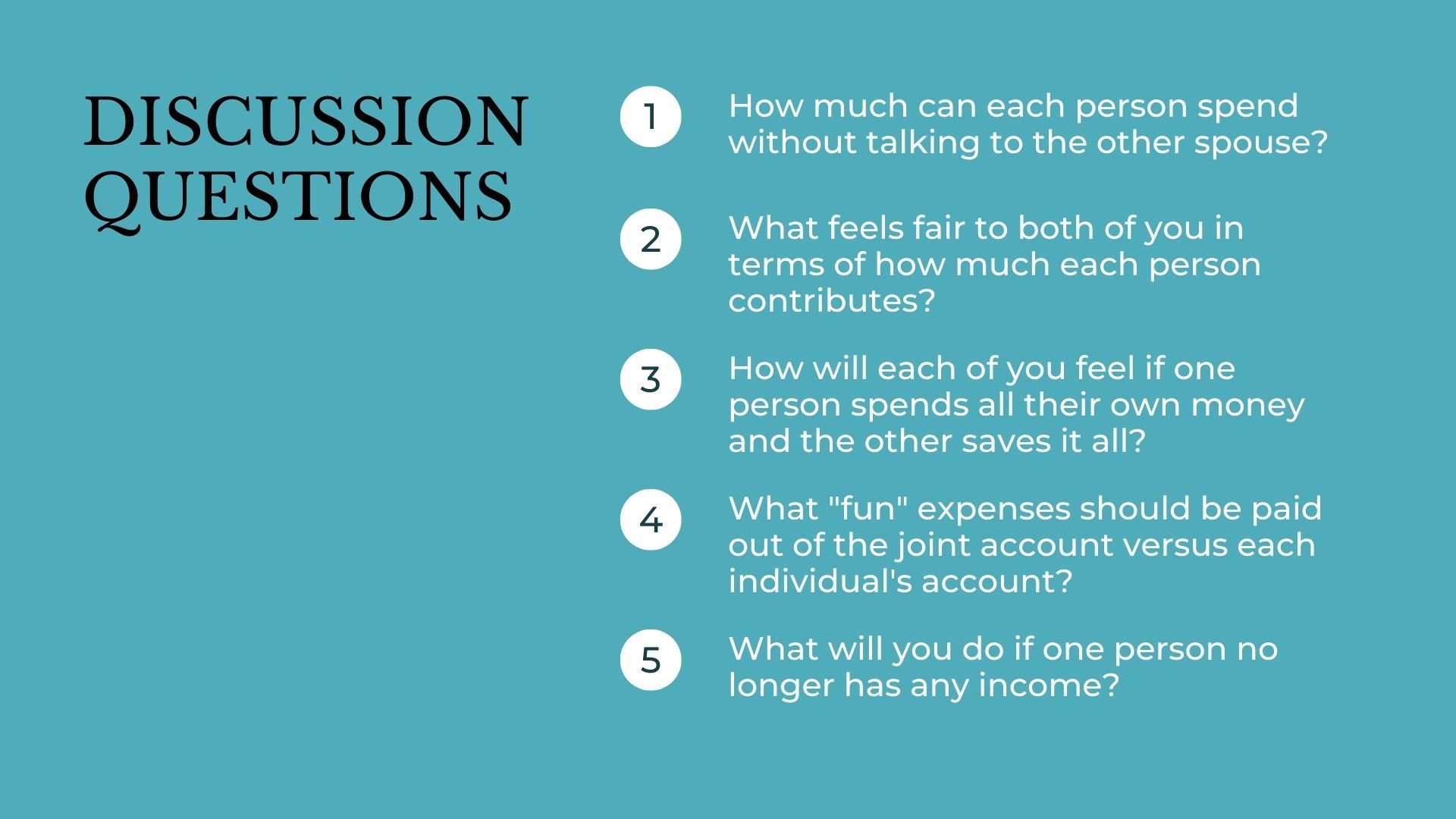

The more you can create guidelines around how spending decisions are made, the better

Above all, partners need to work together to design a system that feels fair and best helps them achieve their dream life together as a couple, in addition to satisfying individual needs and desires.

*Note: these systems address how the couple thinks about and manages money. This may or may not be the same as legal ownership of assets/property as determined by your state.

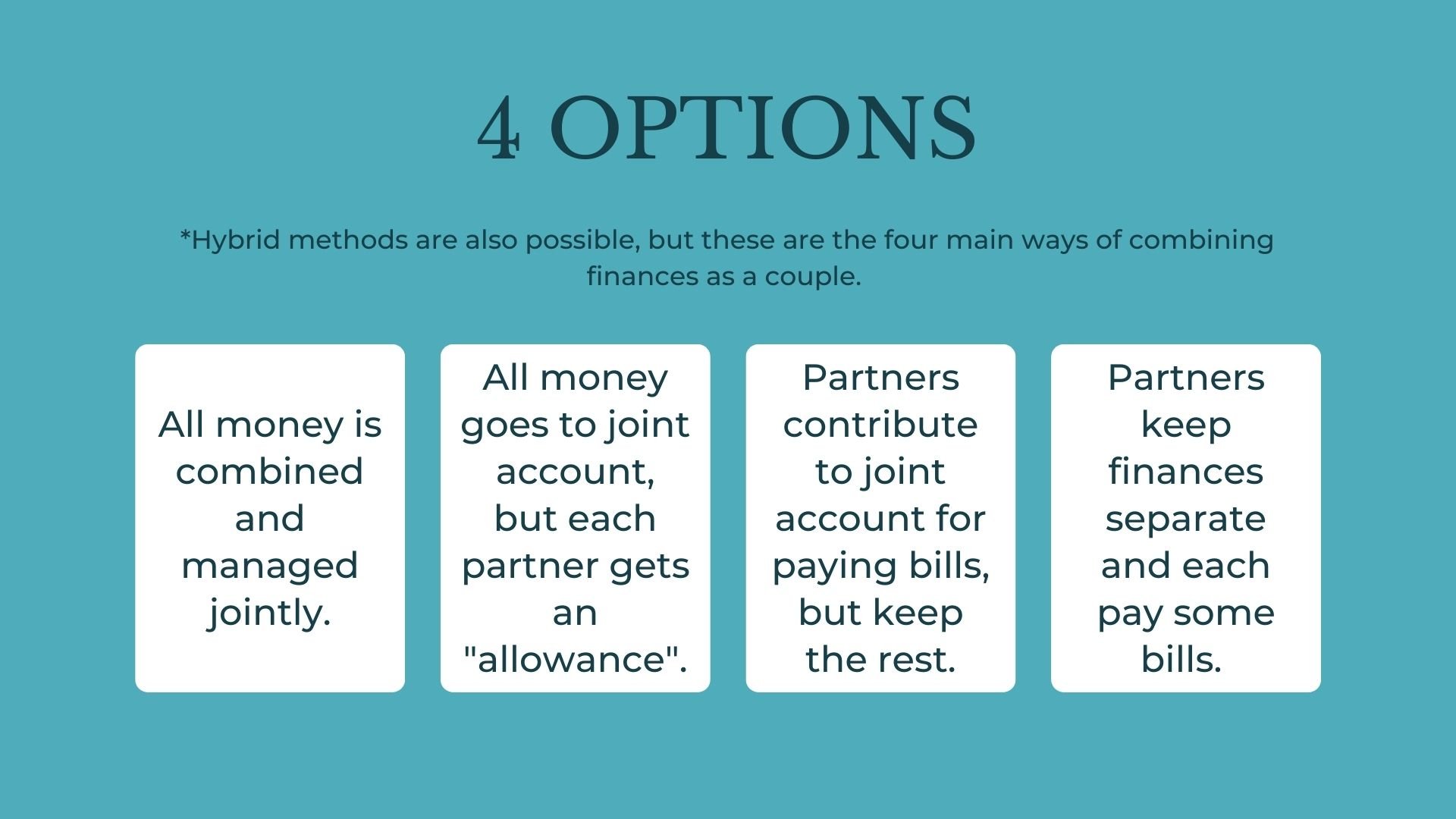

4 Ways Couples Can Combine Finances

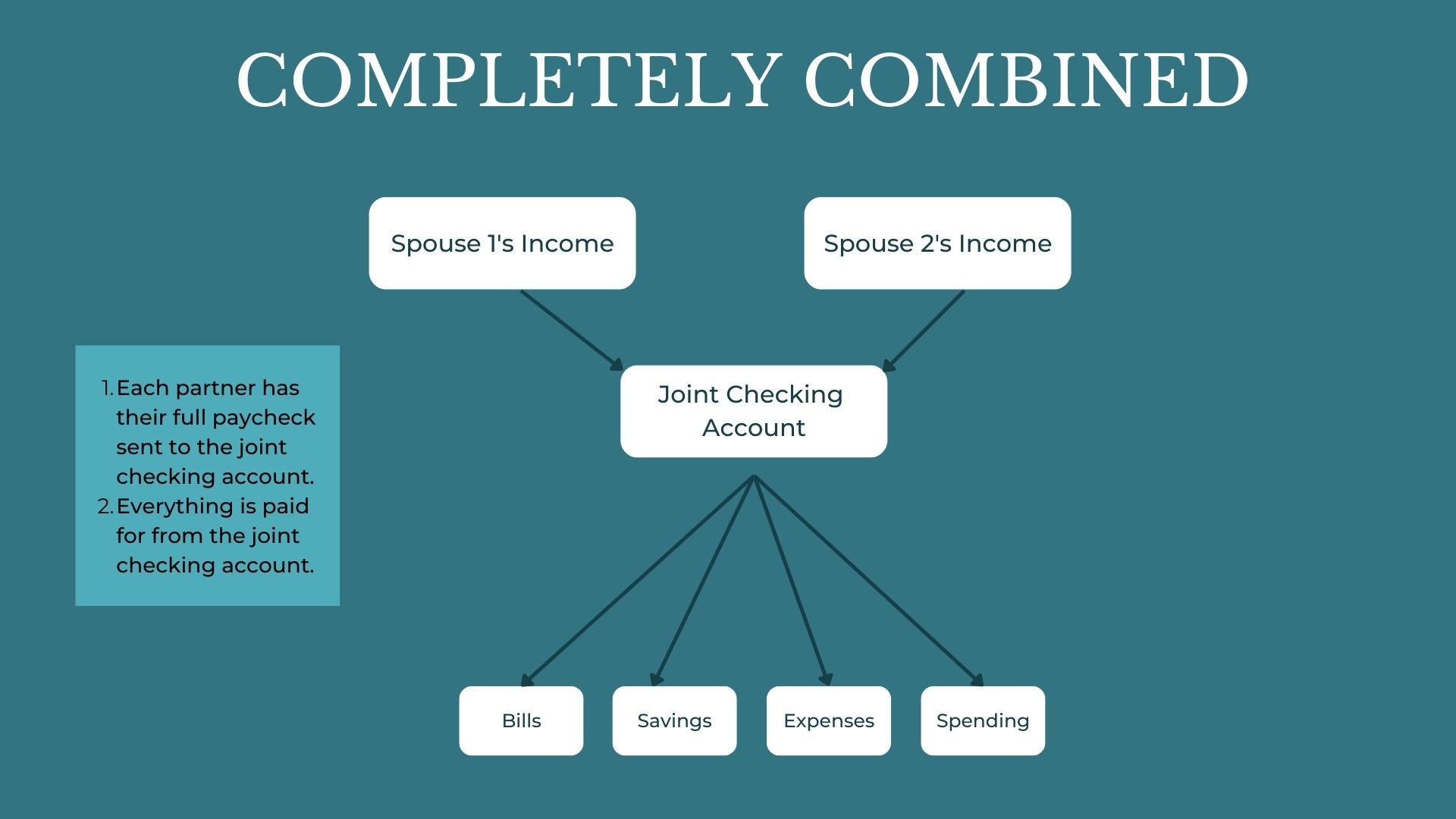

1. Merge everything

As we’ve already discussed, this is the traditional way of doing things, where all assets, accounts, and incomes are merged into shared, marital assets. You combine everything, including debt!

Lest you think this is just a thing of the past: financial guru Dave Ramsey’s website recommends:

“When you get married, you’ve got to combine your money into joint accounts. You’re becoming one, so your finances should too. If you keep this one area separated, it can lead to separation in other areas. Don’t. Go. There. Work together from a shared account to create accountability, honesty and a sense that you’re in this together! Because guess what? You are!” -Dave Ramsey, Ramsey Solutions

Ramsey is absolutely correct that you are a couple now and need to have a sense of being in this together. When you get married, you are entering into a relationship that is more than just one of you. Part of being married is thinking about your finances, goals, and life together, as a couple.

However, merging everything is not the only way to have a shared sense of reality and doing so can be extremely dangerous. It is all-too-common for spouses with merged finances to have only one person making all of the decisions and controlling everything. This often leads to financial abuse.

That’s why I recommend having each spouse have at least some money of their own to spend as they like without having to discuss it. IF you choose to merge all of your finances anyway, it is vitally important to ensure that both partners have equal responsibility for making decisions and managing finances.

Pros of Combining All Finances

It’s simpler because there are fewer accounts and you don’t have to figure out how much each spouse contributes or who pays for what.

It can create an increased sense of being in this together as a couple.

Cons of Combining All Finances

It often leads to a power imbalance because one spouse manages everything and makes all decisions.

It often leads to financial manipulation and abuse.

It can feel unfair when partners are bringing vastly different things into the marriage. For example, one partner brings a huge amount of debt or one partner has significantly higher income or more assets.

It doesn’t work very well when one partner has to pay alimony to a previous spouse.

Having to ask permission to buy every little thing is demeaning and bad for the individual and the relationship.

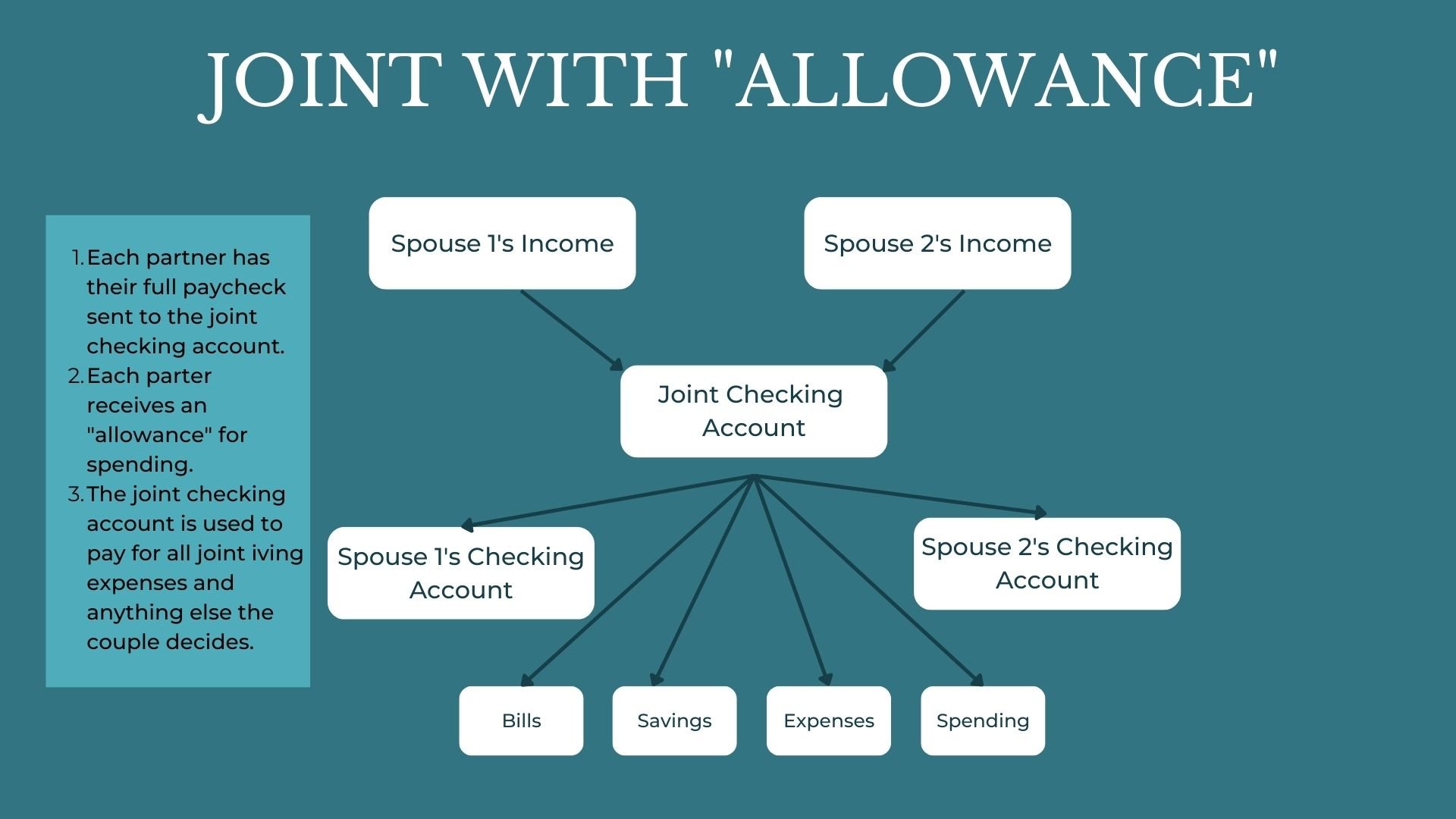

2. Mostly Combined Finances

In this system, all income goes into a joint checking account, but each spouse receives a set amount of money that can be spent in any way they like. It’s sort of like getting an allowance.

Many people, myself included, feel it is important for spouses to have at least some access to their own money. Being able to buy things without a spouse’s approval (within reason) gives each spouse a greater sense of control and can help reduce fights over trivial things. Everyone should be able to spend at least some money in any way they want.

Pros of Mostly Combined Finances

It balances the sense of shared reality that comes with combining finances with giving each partner a small sense of control and freedom.

Sometimes having equal amounts of spending money can reduce feelings of unfairness

Cons of Mostly Combined Finances

One or both spouses might feel like they do not have enough control over the money they earn.

It can cause resentment if one spouse brings in a huge amount of debt or other financial obligations

It may not work if one spouse always wants to spend more of the combined resources than the other.

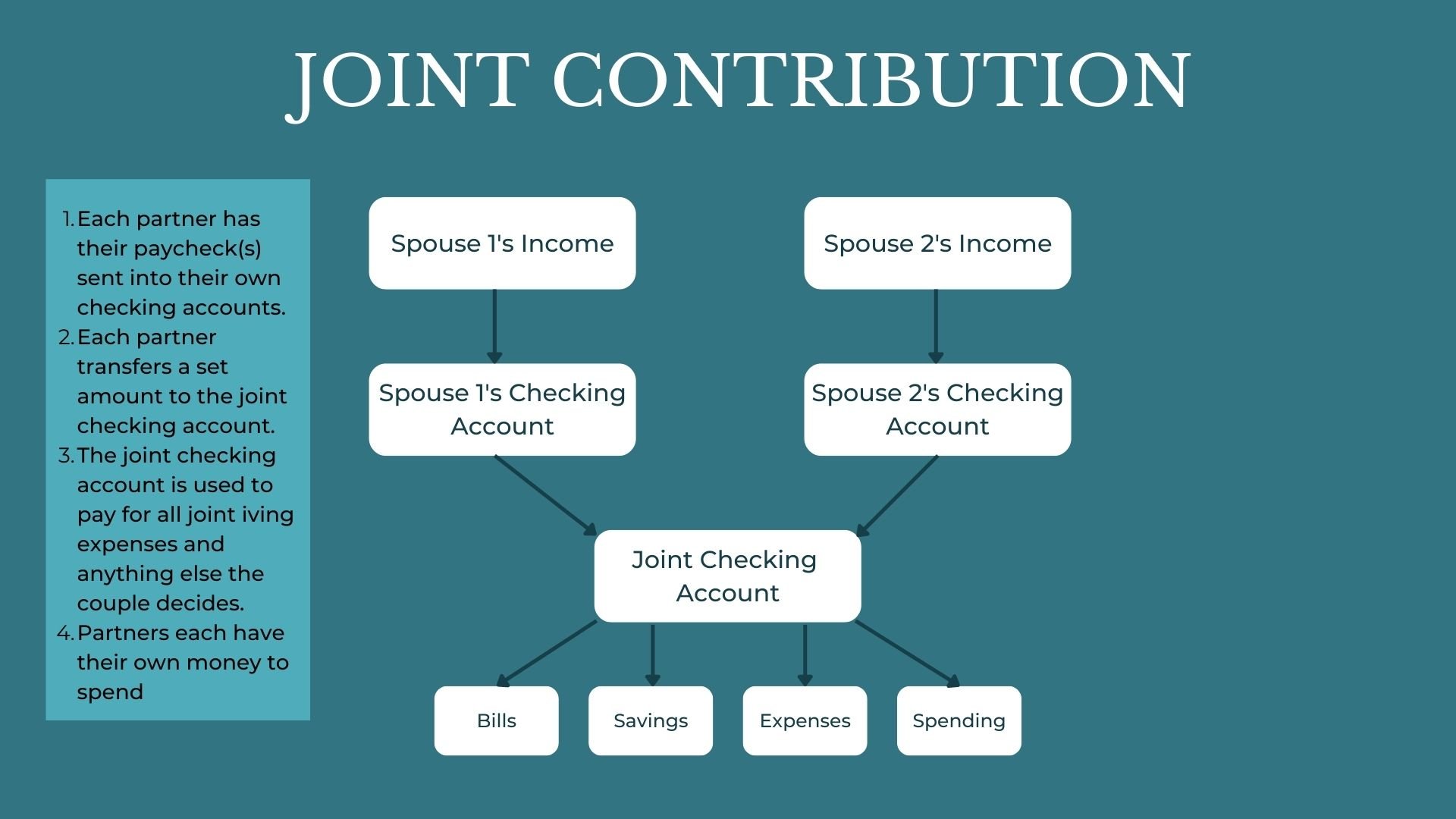

3. Mostly Separate Finances

This system involves each spouse keeping their own income and contributing a set amount to joint finances. All shared bills get paid from the joint checking account, and partners both contribute to joint savings accounts for things like emergencies, vacations, home improvements, or any other shared goals.

Partners keep any assets or responsibility for debt they bring to the marriage. Income beyond what goes to joint finances is theirs to keep.

Pros of Mostly Separate Finances

This system is much easier for couples to manage when they’ve been married before and maybe have kids from another marriage. One spouse doesn’t have to feel like they are supporting their spouse’s ex-spouse.

Each partner has a greater sense of control over their resources.

Each partner has more flexibility to spend what they want without worrying about what the other thinks.

Cons of Mostly Separate Finances

It can be challenging to agree on what is fair when incomes, debt, etc are uneven.

It can lead to disagreements about what should be paid for jointly versus individually.

It can be easy for partners to focus on their own desires at the expense of creating a shared reality as a couple.

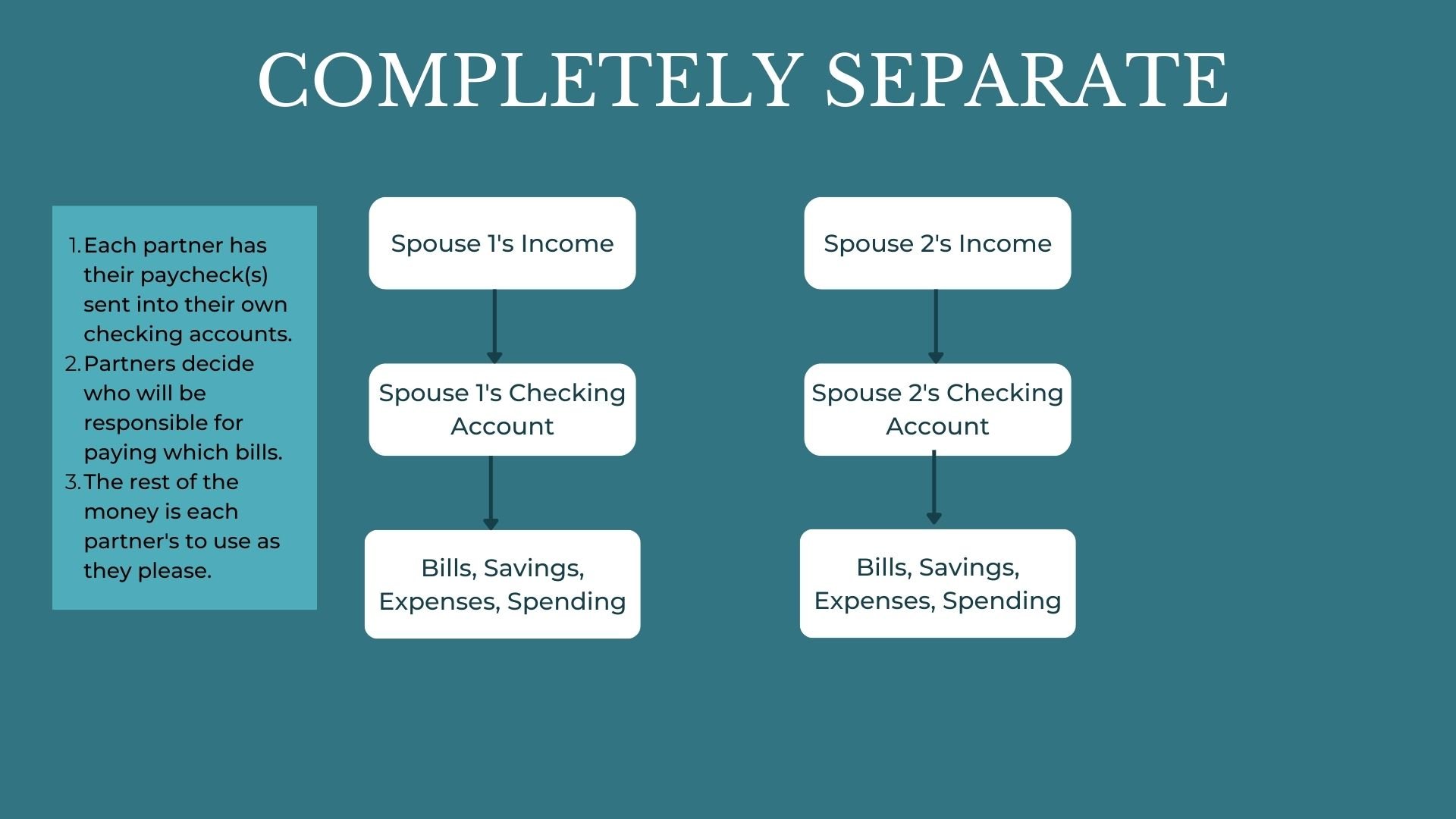

4. Completely Separate Finances

Most couples share finances at least to some extent, but some couples thrive with completely separate finances.

In this system, each partner keeps all of their own money in their own accounts. Bills are divided up and paid by the designated partner.

Pros of Completely Separate Finances

Pin this image to save for later!

It can work well for partners who live together, but don’t have a lot of other shared expenses and like to do things on their own.

It gives each spouse a greater sense of independence and individuality

It can be a good system for partners who live together, but aren’t married.

Cons of Completely Separate Finances

If you have children, it becomes much more difficult to manage because there are so many shared expenses.

It can be hard to think as a couple and work together to build your shared dream life.

It can lead to fights about who will pay for things.

Managing money as a couple is more about how you manage your relationship than it is about the numbers. What’s much more important than how you set up your accounts is that you are both participating in making money decisions and that you communicate about it in a healthy way.

Want help setting up a system that works for you and helps you achieve your dreams? Schedule an appointment!