Is It Worth Consolidating Credit Card Debt?

Debt consolidation can be a useful tool for helping you pay off debt, but it’s not a complete strategy or a guaranteed solution.

Debt consolidation loans are often marketed as a way to "get out of debt faster." You'll notice they stop short of actually promising you'll get out of debt faster (because that's not something a loan can guarantee), but they give that impression by promising to lower your monthly payment and save you money with a lower interest rate. Some companies even tell you that you'll be getting rid of your "bad" debt by consolidating.

(Apparently we're supposed to believe credit card debt is bad, and that a consolidation loan makes it "good." I don't believe in good debt and bad debt. It's just debt. But that's a conversation for another day.)

It's true that a consolidation loan can (and often does) lower your monthly payment and your interest rate. But that is not the same thing as paying off debt faster.

In fact, as a financial counselor, I find that a lot of people who consolidate their debt end up right back where they started — except now they have a personal loan and new credit card balances. Many of my clients come to me for help with their debt after trying to consolidate with a personal loan, HELOC, or 401k loan, because it didn't work.

The problem isn't that consolidation loans don't work. Sometimes they absolutely do. The problem is that a consolidation loan isn't a complete debt solution — it's just one part of the plan.

So if you're wondering whether consolidating your debt is smart, or worth it, or a good idea at all, this post is for you. Keep reading to learn why consolidation works for some people and not others, when it's actually a good idea, and how to use it the right way so it actually helps you get out of debt.

What does it mean to consolidate debt?

Before we talk strategy, it helps to understand what consolidating debt actually means. There are a lot of companies promising things that all sound similar, but the options can be very different — and some of them are a bad idea or an outright scam. I'll point out what to watch for below, but let's start with the legitimate options people actually use.

When we talk about consolidating debt, we usually mean taking debt of one kind and turning it into debt of another kind. You're changing the structure and the terms.

For example, you might take debt spread across several credit cards and turn it into a single personal loan with one payment. Or you might take out a HELOC or a 401k loan to pay off the cards so you only have that one payment to make. It's the same amount of debt — it just has different rules and a different interest rate.

So consolidating your debt doesn't automatically reduce how much you owe. It changes the terms, the payment, the interest rate, and the timeline. It can reduce what you pay over the life of the debt — but only if it lowers your interest rate and you don't stretch the repayment timeline so long that you end up paying more overall.

A note on student loans: Consolidation often comes up with student loans. Private student loans can be combined and/or refinanced at a lower rate. But federal student loans are a special category with their own rules and protections, and consolidating them can cost you those protections. Please work with a student loan expert before consolidating federal student loans so you fully understand the consequences.

Types of debt consolidation

When people talk about consolidating debt, they're usually referring to one of these:

Personal loans and debt consolidation loans

You take out a loan for a set amount and use that lump sum to pay off your credit cards, buy now pay later balances, or other high-interest debt. A debt consolidation loan is a type of personal loan that can only be used to pay off other debt. A regular personal loan can be used for other things too, like a wedding or a big purchase.

Balance transfer cards

These are credit cards that offer a promotional period with a low interest rate — sometimes as low as 0%. You move high-interest credit card debt onto the card and use that window to pay it down without racking up as much interest.

Two things to watch for: most cards charge a balance transfer fee (usually 3–5% of the amount you move), and when the promo period ends, the rate jumps back up — often higher than you'd expect.

These work best when you can realistically pay off most or all of the balance before the promo period is over — and keep in mind you usually need good credit (often a score around 670 or higher) to qualify for the best offers.

Home equity loans and HELOCs

If you have equity in your home, you may be able to borrow against it and use the money to pay off higher-interest debt. These often come with a lower interest rate because they're secured by your home — though a HELOC's rate is usually variable, which means it can climb over time. That's also the risk you can't ignore: if you can't make the payments for any reason, you could lose your house.

*One thing to understand is that you're converting unsecured debt (credit cards) into secured debt backed by your home. If you can't make the payments, your home is now part of the equation.

401k loans

Most 401k plans let you borrow from yourself, and you pay the interest back to your own account. That can help you pay off debt at a lower cost, and it beats taking an early withdrawal (where you'd lose money to penalties and taxes). They're usually easy to set up through your HR department.

The risks: your money is out of the market and missing out on growth, and if you leave or lose your job, you'll generally have to repay it (or roll over the balance) by the due date of your next tax return. If you don't, the unpaid amount gets treated as an early withdrawal — meaning you'll owe taxes on it, plus a 10% penalty if you're under 59½.

Debt management plans

A debt management plan isn't technically consolidation, but the result is similar: reduced interest rates and one (hopefully lower) monthly payment.

These are run by nonprofits who negotiate lower rates on your behalf. You make one payment to them, and they make sure each of your lenders gets paid. You'll usually work with a credit counselor to build a budget, and you're typically required to close your credit cards — which can lower your available credit and temporarily ding your score. Even so, these programs can be a lifeline.

The National Foundation of Credit Counseling is a good resource for finding reputable and trustworthy programs.

Note: Debt management plans are not the same as debt settlement companies. Debt settlement companies are usually for-profit, charge high fees, and often push you into collections so they can try to settle your debt for less. Be very careful with any company promising to help you pay off your debt — there are a lot of scammers, and even the ones that aren't technically scams can leave you worse off than before.

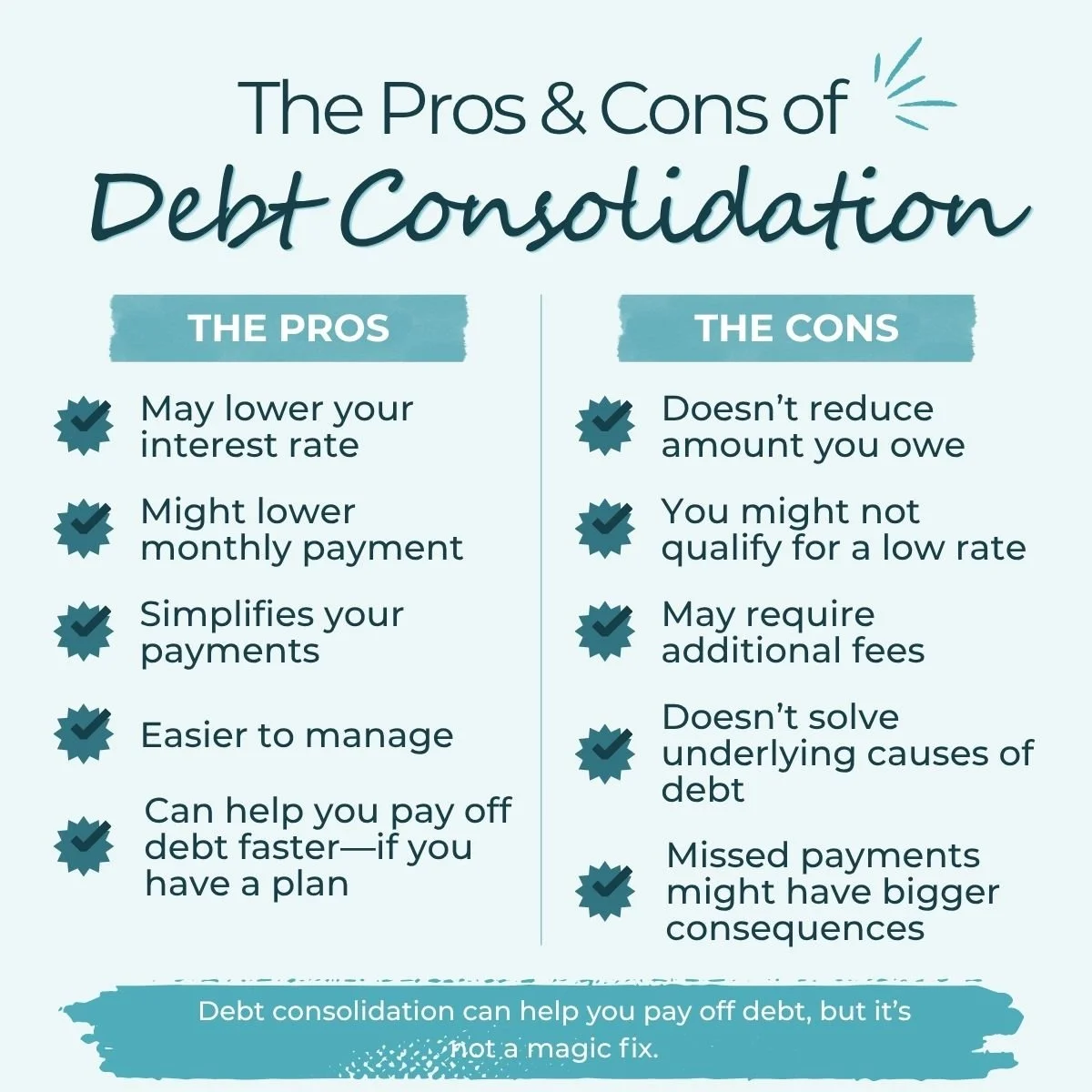

Why debt consolidation works for some people

Debt consolidation has helped a lot of people get out of debt. A lower interest rate can save you real money over time, and a single lower payment can free up some breathing room in your budget.

One thing to watch, though: a lower monthly payment on its own can actually mean a longer timeline and more interest. The real savings come from a lower interest rate, not just a smaller payment. (Either way, the amount you owe stays the same — you're just changing the terms.)

One payment also makes life simpler. The more separate payments you have, the harder everything is to track and plan around — especially with buy now pay later balances scattered everywhere. Going from five payments to one makes your debt far easier to manage and stay on top of.

When debt consolidation is a good idea

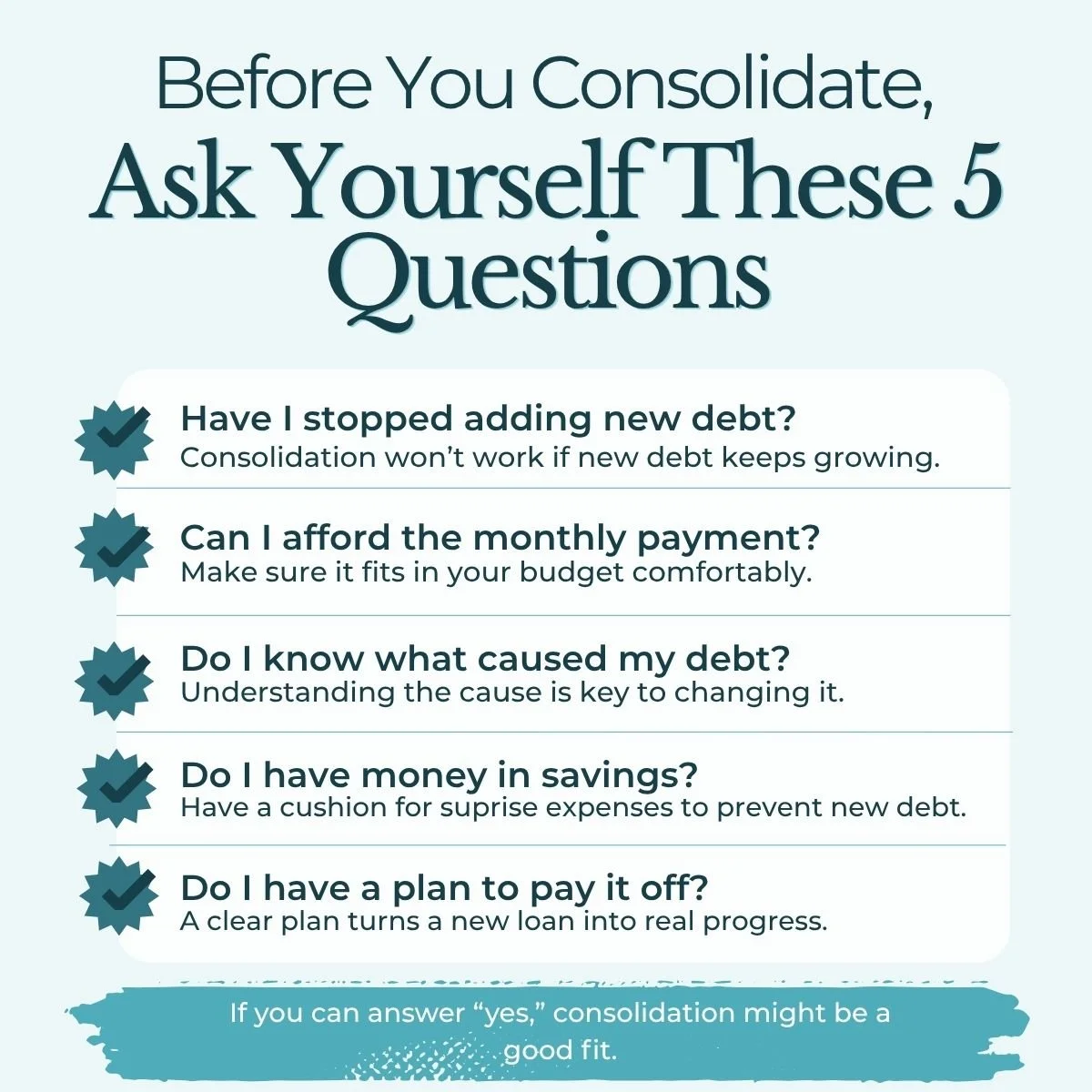

Consolidation can be a great tool, but it's not right for everyone. It tends to work when these things are already true:

You've stopped adding new debt (or you have a real plan to).

You understand what caused the debt in the first place.

Your income covers your current expenses.

You have a plan for unexpected expenses — even a small emergency fund or buffer.

You can qualify for terms that actually save you money — a lower rate, without stretching the timeline so far that you pay more overall.

You have a debt payoff strategy beyond the loan itself.

If most of those are true, consolidation can genuinely help. If they're not yet, that's okay — it usually just means consolidating right now would move the debt around without fixing what's creating it. More on how to get ready for that below.

Why debt consolidation sometimes doesn't work

When consolidation doesn't work, it's almost always because it got treated as a standalone fix. The single biggest mistake I see is expecting the loan to solve the problem all by itself.

A realistic example

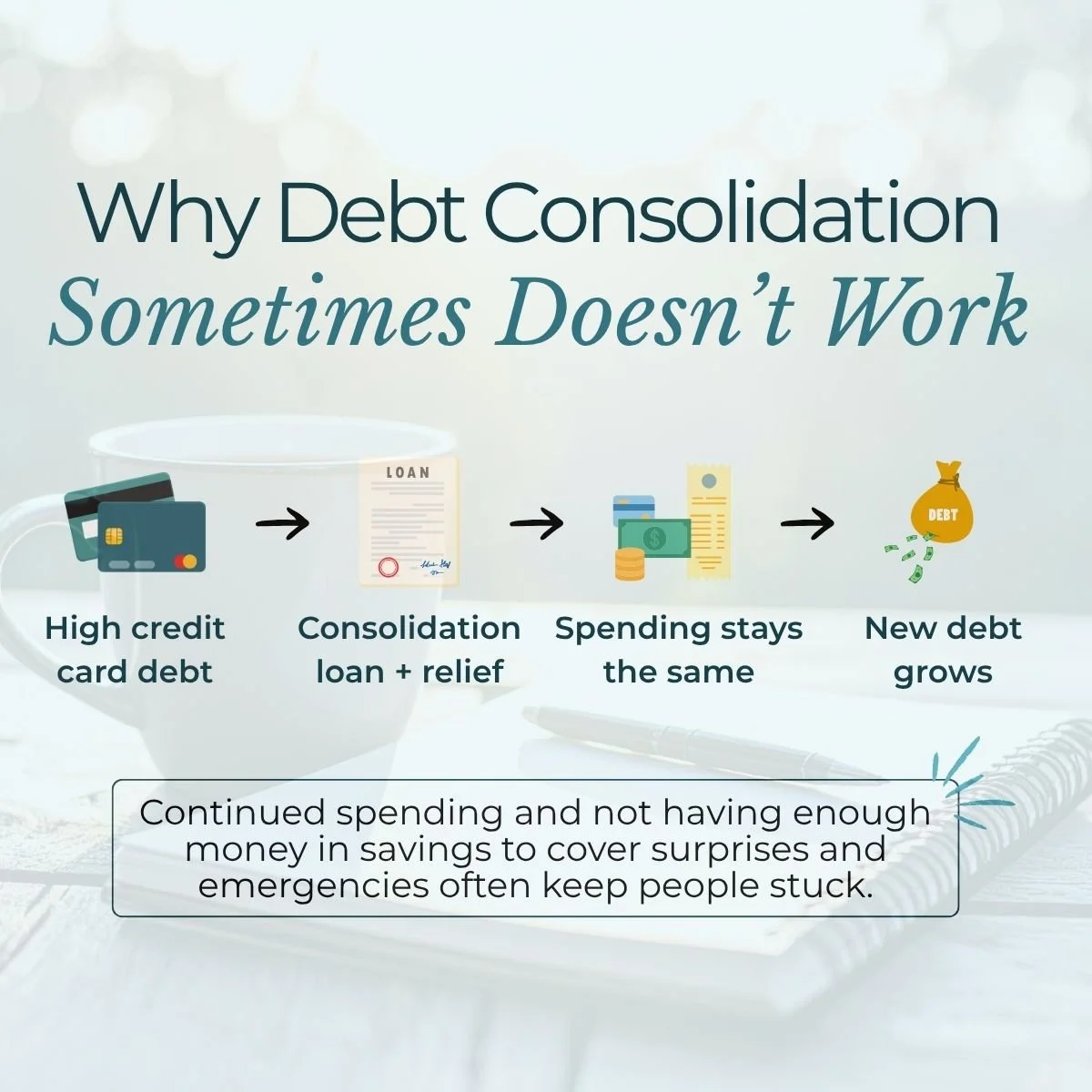

Say you have four credit cards with a total balance of $33,046 and minimum payments adding up to about $945 a month.

You take out a consolidation loan and use it to pay off all four cards. Now you have one payment instead of four, a lower interest rate, and a simpler plan. That's a real benefit.

But what happens next matters a lot more than the loan.

If six months later you put a car repair on a credit card, then a vet bill, then the holidays, those balances start creeping back up. Before long, you've got a consolidation loan and new credit card debt.

The loan didn't fail. It did exactly what it was supposed to do.

The problem was that nothing changed about the circumstances that created the debt in the first place.

Here's the part that's hard to hear: consolidating often feels like you're doing something about your debt, when really you've just moved it around and changed the terms a little.

There's always something that caused the debt. Sometimes it's a one-time event — a big medical bill, a layoff, an emergency. In that case, consolidation has a better shot at working, because the debt is done and there won't be more piling on.

But often the cause is ongoing: living expenses that are too high for your income, not knowing where your money goes or how much you can safely spend, one too many surprise expenses. These things happen to so many people, and you shouldn't be embarrassed — often it isn't even your fault.

But if you don't stop whatever is causing the debt, consolidation won't work.

What to do first so consolidation actually works

Before you consolidate, two things make the difference between this working and you ending up right back where you started:

Create a spending plan that covers your living expenses and your debt payments without taking on new debt.

Save a little money first — a starter emergency fund with some wiggle room — so the next surprise doesn't land on a credit card.

Once those two things are in place, consolidating your debt becomes much more likely to actually work. Depending on the type of consolidation you choose, the consequences of missed payments can be more severe than they would be with unsecured credit card debt.

Does consolidating debt help or hurt your credit?

Both can happen, and it mostly depends on what you do afterward.

In the short term, applying for a new loan or card usually causes a small, temporary dip because of the hard credit inquiry. If you close credit cards after paying them off, that can ding you too — it lowers your total available credit, which can raise your credit utilization (the percentage of your available credit you're using).

Over time, though, consolidation can actually help. Moving balances off maxed-out cards lowers your utilization, and a steady history of on-time payments on your new loan builds your score back up. So the early dip is often worth it — as long as you don't run the cards back up.

One thing to know if your credit score is already low: you can often still qualify, but the rate you're offered may be much higher than the rates you see advertised online. Always compare the actual rate and the total cost before you accept anything. A consolidation loan at a worse rate than what you already have isn't worth taking.

Ultimately, the most important thing is that you are able to make your payments. Consolidating your debt only to default on the payment can actually be worse than if you paid less on your credit card balance.

Alternatives to debt consolidation

Consolidating with a loan or balance transfer card can be a great way to pay off debt faster, but it's not your only option. You can also:

Call your lenders to negotiate a lower interest rate or ask about a hardship program

Use a nonprofit debt management plan

Aggressively pay it off by cutting expenses, earning more, and using a debt snowball or avalanche

File for bankruptcy

Learn more about debt payoff strategies (including some you should avoid) here:The Best Ways to Pay Off Credit Card Debt

How to consolidate debt

Decided it's worth a try? Here's how to do it without getting burned.

Start by listing all of your debts — the balance, interest rate, and minimum payment for each one. You'll use this to compare your current debt against any offer you get, so you can actually see whether it's a better deal.

Then look at your options. Depending on your credit, income, and whether you own a home, you might qualify for:

A personal loan

A balance transfer credit card

A home equity loan or HELOC

A debt management plan through a nonprofit credit counseling agency

Before you accept any offer, compare the interest rate, the monthly payment, the fees, and the total amount you'll pay over the life of the loan. A lower monthly payment can hide a higher total cost if it stretches your timeline way out.

And most importantly, make a plan for what happens after. A consolidation loan can make your debt easier to manage, but it won't fix overspending, a cash flow problem, or a lack of savings. Those have to be handled separately — otherwise the debt just comes back.

Debt consolidation can be a useful tool, but on its own it isn't a debt payoff strategy. It's one piece that can help you move faster. The people who have the most success aren't just changing the type of debt they have — they're changing the habits and patterns that created it.

And that's the hard part. Not because the logistics are complicated (though they can be), but because changing these patterns is emotionally hard. If you want help making a plan, looking at the numbers honestly, working through the emotional side, and staying on track, that's exactly what I do as a financial counselor.

Not sure whether debt consolidation would actually help in your situation? That's where an outside perspective can be useful.

Schedule a free call with me and we'll talk through your situation.

Frequently asked questions about debt consolidation

Does debt consolidation affect your credit score?

It can, both ways. A new loan or card usually causes a small, temporary dip from the credit inquiry, and closing paid-off cards can lower your score by reducing your available credit. But if consolidation lowers your credit utilization and you make consistent on-time payments, it can improve your score over time.

Can I consolidate debt with a low credit score?

Possibly. The lower your score, the harder it is to qualify for good terms, and the rate you're offered may be much higher than what's advertised. Always compare the total cost of the loan before accepting an offer.

Are debt consolidation companies legitimate?

Some are, some aren't. Be especially careful of any company that guarantees results, pressures you to stop paying your creditors, or charges large upfront fees. Research carefully before working with anyone.

Should I use a HELOC or 401(k) loan to pay off debt?

These can make sense in certain situations, but they carry real risk. A HELOC puts your home on the line if you can't make payments. A 401(k) loan can create problems if you leave your job, and it slows the growth of your retirement savings. Make sure you fully understand the tradeoffs before moving forward.

Do debt consolidation loans actually work?

Yes, debt consolidation loans can work. The loan itself isn't what determines success. The people who benefit most are those who stop adding new debt, address the issues that created the debt, and use the loan as part of a broader debt payoff plan.

This article is general education, not personalized financial, tax, or legal advice. Your situation is unique, so please consult a qualified professional before making decisions about your debt, retirement accounts, or taxes.