CDs vs High Yield Savings Accounts: Which Is Better?

If you’ve been wondering how to make your money work harder for you, you might be thinking about CDs vs high yield savings accounts and which is better for your financial goals.

Both are great options when it comes to saving and earning money, but it's important to understand the differences between the two so you can choose the right financial strategy for your needs.

Before we get into the pros and cons of CDs vs high yield savings accounts and what they are, I want you to congratulate yourself for even considering this question. The fact that you're thinking about this means you're already prioritizing saving—and that matters a lot more than which specific account you end up choosing.

Many people spend way too much time trying to find the perfect option, comparing interest rates, and even jumping from one account to another to get the highest rate. Or, they become overwhelmed with figuring out which option to choose and end up doing nothing.

It’s important not to overthink this decision. CDs and high yield savings accounts are both great options. Both keep your money safe and help it grow more than a traditional savings account.

Keep reading to learn what the difference is and what to consider when making your decision.

High Yield Savings Accounts

High Yield Savings Account: How does it work?

High yield savings accounts (HYSAs) are simply savings accounts that pay you more in interest than a traditional savings account. When you signed up for a checking account at your bank, you probably got a savings account as well. These “traditional” savings accounts often pay you next to nothing when you keep money in your account.

For example, basic Wells Fargo savings accounts currently pay .1% in interest (as of Feb 2026 in my zip code). That’s nothing. What’s worse is that Wells Fargo charges you a $5/month service fee unless you jump through the appropriate hoops. That means you’re paying money for the privilege of earning a few pennies.

HYSAs used to be mostly associated with online-only banks, and online banks do still tend to offer the most competitive rates. But many traditional banks and credit unions now offer them too. The institutions that pay the most are generally those that are actively competing for deposits — online banks often lead here because they have lower overhead without physical branches to maintain, and they pass some of that savings on to you.

Large national banks, on the other hand, already have enormous customer bases and less pressure to compete — which is often why their rates lag behind.

Are high yield savings accounts safe?

Yes. Most high yield savings accounts are offered by banks that are FDIC insured or credit unions that are insured by the NCUA.

This means that your money is protected up to $250,000 per depositor per bank by the federal government in case a bank or credit union fails.

Anytime you open a new account, you should check that any bank or credit union you’re considering is covered by the FDIC or NCUA.

Learn more about choosing a bank here.

How much do high yield savings accounts pay?

Interest rates fluctuate depending on market conditions and the federal funds rate set by the Federal Reserve.

So if you want to know how much high yield savings accounts pay, the best thing to do is Google it. Sites like Bankrate.com and Nerdwallet.com regularly update lists of banks with the highest interest rates. And remember, these rates fluctuate, so your rate may go up and down as the economy changes.

Who should use a high yield savings account?

Almost anyone who has savings sitting somewhere earning less. A HYSA is especially good for:

Money you're keeping as a financial backup (what most people call an emergency fund)

Savings for specific upcoming expenses—a vacation, home repairs, a new car, holiday spending

Any money you might need access to in the next few years

Learn more about saving money for upcoming expenses here.

The one thing a HYSA is not good for is long-term retirement savings. The interest rate, while much better than a traditional savings account, still won't grow your money fast enough over decades. That's what investing is for.

One note: the interest you earn in a HYSA is taxable income, so you'll receive a 1099 form at tax time if you earn more than $10 in interest during the year.

CDs (Certificates of Deposit)

CDs: How do they work?

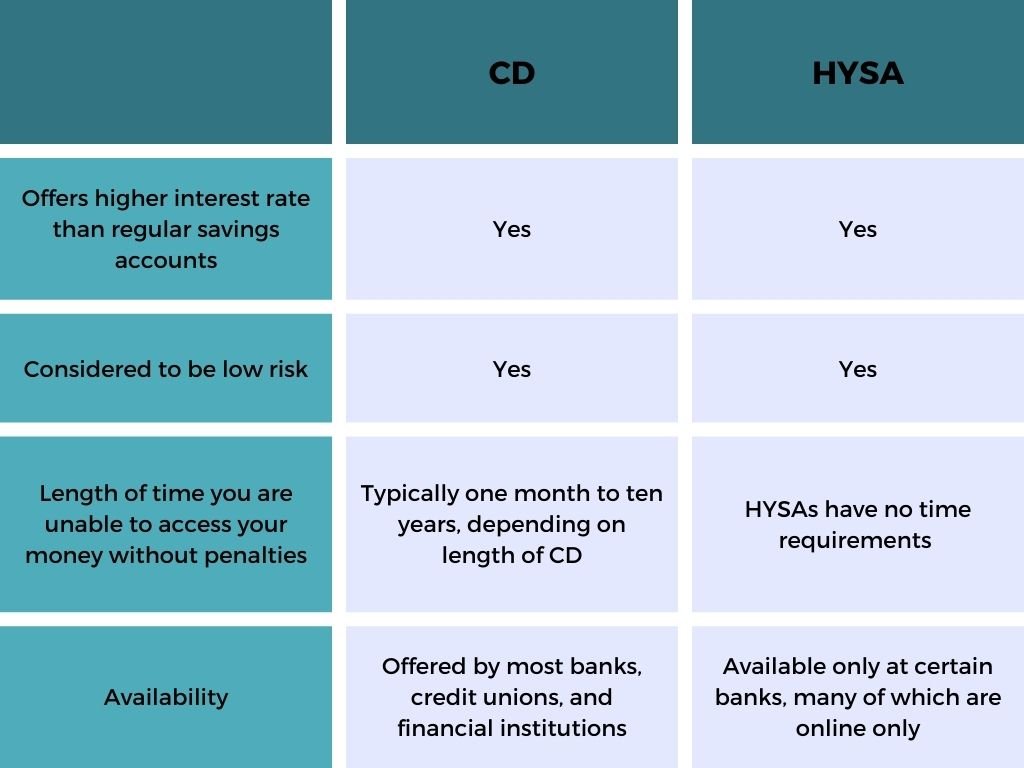

A CD is a savings product where you agree to leave your money with the bank for a set period of time — anywhere from a few months to several years — in exchange for a fixed interest rate. For example, if you put $1,000 in a 1-year CD at 4%, you'll earn $40 in interest by the end of the term.

The tradeoff is that your money is locked in. If you need to withdraw it before the term ends, you'll typically face an early withdrawal penalty. So CDs are only a good fit when you're confident you won't need the money until the term is up.

How much do CDs pay?

Top CD rates as of early 2026 are around 4% to 4.3% APY depending on the term and institution, which means CDs and HYSAs are currently offering very similar rates. This is actually a notable shift from periods when CDs offered meaningfully higher rates in exchange for locking up your money. Right now, you're not always giving up much flexibility for a higher rate.

To find current rates, check with your current banking institution to see what they offer. Otherwise, check with Bankrate.com or NerdWallet to find the best rates currently available.

Are CDs safe?

Most CDs, like high yield savings accounts, are insured by the FDIC or NCUA, meaning that your money is protected up to $250,000. Again, it’s always worth it to check the institution that offers the CD to make sure.

The biggest risk when it comes to CDs is related to tying up your money. When you purchase a CD, you face penalties if you try to remove the money before the term is up. This means that you shouldn’t buy a CD unless you are reasonably certain that you will not need the money during that time period. Penalties vary, so read the fine print before committing if you’re unsure.

Another potential problem (or benefit!) when buying a CD is that you are locking in a particular interest rate. If interest rates keep rising, you could be missing out on earning even more in interest (which would be the downside). On the other hand, if interest rates go down after you purchase the CD, you’re locking in a higher rate than you otherwise could get.

For example, let’s say that I purchase a 1-year CD at 4%. If interest rates go up to 6%, I might be missing out on the opportunity to buy a CD at 6%. If the interest rates for new CDs go down to 2%, I’d feel pretty good about having my money locked in at 4%. (This is also one of the potential benefits of CDs over HYSAs—if interest rates go down, a CD might give you a higher rate for longer.)

To hedge against this risk, some people use a strategy called a CD ladder. Some institutions have technology that can set this up for you and walk you through the process. Otherwise, a financial advisor can help you determine if that’s a good strategy and help you get started.

Who should purchase CDs?

CDs make the most sense in two specific situations:

1. You want to lock in a rate before rates drop. CD rates are fixed for the entire term. If you think interest rates are going to decline — which is a reasonable expectation given that the Fed cut rates three times in late 2025 and may continue — a CD lets you lock in today's rate for longer. Your HYSA rate will fluctuate with the market; your CD rate won't.

2. You have money you know you won't need for a specific period of time. If you're saving for something that's 1-2 years away and you're confident you won't need to touch the money, a CD can work well. The fixed rate and defined timeline can feel satisfying if you're the kind of person who likes knowing exactly what you'll earn.

HYSA vs. CD: Which is right for you?

Choose a HYSA if:

You might need access to the money at any point

You want something simple and easy to manage

You're not sure how long you'll be saving

You want flexibility as interest rates change

Consider a CD if:

You have money you're confident you won't need for a defined period of time

You've found a rate you want to lock in before rates decline further

You like the predictability of a fixed rate and a fixed timeline

When it's probably not worth it: If the CD rate is only slightly higher than the best HYSA you can find, the tradeoff of locking up your money usually isn't worth it. Right now, with CD and HYSA rates running close together, the flexibility of a HYSA wins for most people in most situations.

Other options for saving cash

A HYSA and a CD aren't your only options. If you have a larger amount saved or want to explore further, a few others are worth knowing about.

Money market accounts work similarly to HYSAs — your money stays accessible and earns interest. Some come with check-writing privileges or a debit card, which can be convenient. Rates are comparable to HYSAs, so it's worth comparing if you come across one with a better rate.

Treasury bills (T-bills) are short-term government securities — essentially you're lending money to the US government for a set period of time in exchange for interest. They're currently competitive with HYSA rates, and one potential advantage is that the interest is exempt from state and local income taxes, which can matter depending on where you live. The tradeoff is that they're slightly more involved to set up than a savings account.

Money market funds are different from money market accounts — these are investment products, not bank accounts, and they're not FDIC insured. They can offer competitive rates but come with a bit more complexity. Worth knowing they exist, but probably not where most people need to start.

For most people, a HYSA covers everything they need. But if you have a significant amount in cash savings and want to optimize further, exploring these options, ideally with a financial planner, could be worthwhile.

Next steps

If your money is sitting in a traditional savings account earning close to nothing, look into opening a HYSA. Check Bankrate.com or NerdWallet.com to compare rates and find an account that's FDIC or NCUA insured.

If you already have a HYSA, consider whether current CD rates make sense for any money you're confident you won't need for a year or more.

Make a decision and get started. Don't let the pursuit of the perfect account stop you from doing something.

In the end, the best savings account is the one you actually put money in.

Read Next: Is a High Yield Savings Account the Best Place for My Money After Paying Bills?